Europe’s Need for Space Sovereignty: Spacecraft

This continues an analysis comparing Europe’s desire for space sovereignty versus what it is actually doing. I concluded that while Europe’s space managers keep mentioning space sovereignty in their chant circles, they have a history of underwhelming accomplishments, especially in developing their launch industry. Making matters worse is that the industry competitors have changed, and the political situation is placing Europe in a highly untenable position.

I also noted it’s not all bad news–although some might consider it mixed.

Growing Spacecraft Deployments

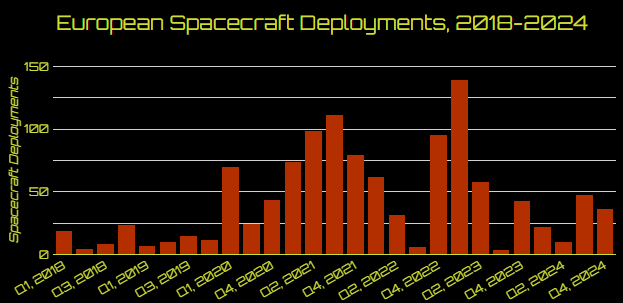

With such a low launch cadence, it’s possible that Europe’s single launch service, which launches only three rockets annually, is missing out on customers. Indeed, the satellite deployment data shows a few instances of this; over thirty European nations deployed more than 1,150 spacecraft from 2018 to 2024.

The bar chart shows Europe’s spacecraft deployment rise and decline. However, it should be mentioned that between the first quarter of 2020 and the first quarter of 2022, most spacecraft deployed were OneWeb internet relay satellites. During that time, all OneWeb satellites were launched on Soyuz rockets–two launches from Kourou in French Guiana and the remaining 11 from Kazakhstan or Russia. The rise in spacecraft deployments from Q4 2022 through Q2 2023 also consisted primarily of OneWeb satellites, but they were launched on Indian and U.S. rockets.

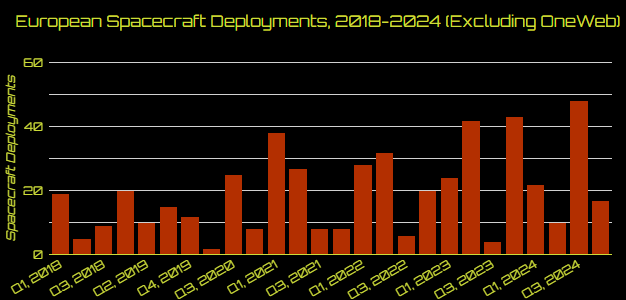

Excluding OneWeb deployments reveals a growth trend for European spacecraft deployments.

That increase means that most European spacecraft operators used rockets that weren’t European (or Russian) to deploy their satellites for the last two years (2023-2024). That’s the bad news part of this story–for whatever reason, unavailability, cost, reliability, etc., European satellite operators chose a European launch competitor. Their choice to do so was for the good of their businesses, not because they were anti-European or against European space sovereignty.

The Positive Spin

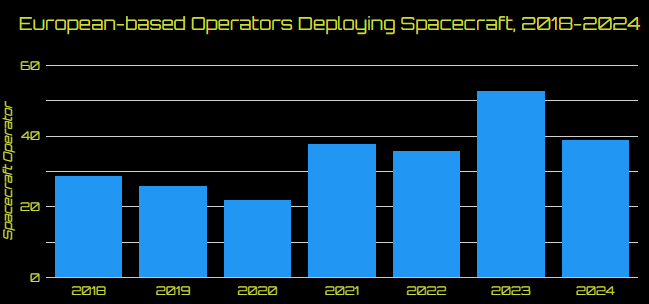

However, this is also a good news story. During that time, nearly 160 European-based businesses and organizations deployed those spacecraft. Also, at least in those six years, there was a (more or less) upward shift in the number of European spacecraft operators that deployed spacecraft. However, while the trend is upward, there were some declines, including from 2023’s high of nearly 55 operators to almost 40 in 2024. Despite Europe only conducting three launches in 2023 and again in 2024, more European spacecraft operators deployed spacecraft during those same years.

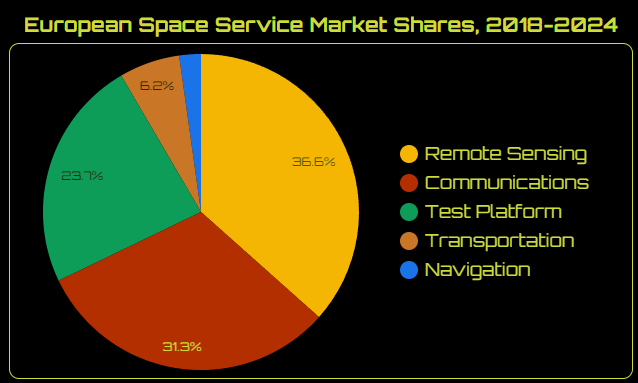

Those spacecraft operators also deployed satellites that provided a range of services. Like the U.S. spacecraft operators and Starlink, OneWeb satellites obscure the European service market shares. Without OneWeb, the shares of satellites with services provided by the various European operators are below.

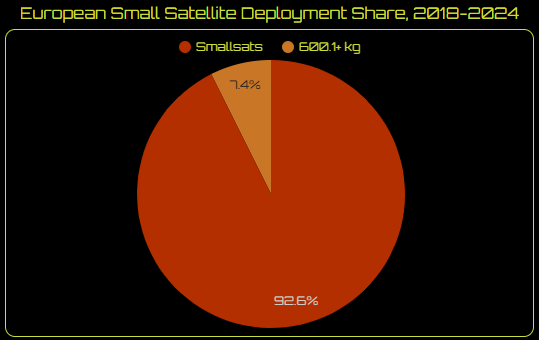

It seems European satellites provided a decent range and number of services. The Europeans also used them to test other concepts, as seen by a high share of satellites used as test platforms. That is unsurprising because most of the satellites Europeans deployed were small satellites–nearly 93%.

Is it strange that Europe’s launch capability is almost non-existent, but its satellite manufacturing, operators, and services are so robust? I suggest that smallsats play a large part in European spacecraft diversity. Smallsat buses require compromises that appear acceptable to European and other operators worldwide.

Europe’s Sovereignty Conundrum

Here’s the kicker: many European smallsat operators didn’t use smallsat launchers from 2023-2024. They used rockets that offered rideshare services. That trend suggests that European companies developing smallsat launch services should knock themselves out of the delusion that they will somehow become competitive with rideshare services. European space sovereignty and those smallsat launch venture investors can’t afford not to have several more capable launch systems.

Europe’s space industry inadvertently juxtaposes launch services and spacecraft operators, providing interesting information. The number and growth of spacecraft operators show a hunger for spacecraft-provided services (or at least a perceived hunger by the operators). Their activities are building an ecosystem that will probably make building smallsats less expensive as the supply chain for them grows. The diversification of payloads and services indicates a healthy industry that is still researching the possible services only spacecraft can provide.

Like U.S. government space stakeholders, the European Union and ESA initially relied on legacy spacecraft manufacturers (it looks like they still do). In the meantime, space sovereignty for Europe’s spacecraft operators seems to be establishing itself, largely thanks to commercial services (over 84% for the period). This is not to downplay ESA’s accomplishments, but its spacecraft deployments tell a story, indicating its activities are not as relevant as they once might have been.

Whether the growth of European spacecraft deployments and operators continues is uncertain. It’s entirely likely that European space operators would instead deploy their spacecraft on European-made and operated rockets. It may well be that the constriction of European launch services will eventually impact their growth. Some may leave Europe for alternatives that will give their businesses a chance to thrive.

It’s a dilemma for you, Europe. It’s one I don’t envy.

Relying on one U.S. launch service in today’s world is asking for trouble. Relying on one specific company to develop launch capability for European space sovereignty hasn’t worked out well, either. Europe needs more than words and memos. It needs orbital launchers to attract its European spacecraft operators and others. A way to achieve this needs to be found and then implemented.

A word of caution, however: while some might view NASA’s resupply program as inspired, resulting in the Falcon 9, I suggest that was not the case. NASA didn’t go all the way. It was also initially uninterested in reusability. Sure, Northrop Grumman (or Orbital ATK or Orbital Sciences) provided Antares. But all U.S. spacecraft operators still rely pretty much on one company, SpaceX, for a ride to space.

That’s unhealthy, no matter how well SpaceX is doing currently.

Europe must develop a launch capability that is more comprehensive and better than that. Perhaps not to the breadth of China’s launch offerings, but then again, why not?

Look, I get it…you’re an amalgamation of cultures, languages, and governments. One country might totally dig space science while another ten couldn't care less. Use your amalgamation as a strength. Learn not just from your competitors' successes but their weaknesses, too (that whole SWOT thing). Learn from ALL of your potential customers’ needs, not just the high-paying ones who require a launch once or twice a year. You once decided you wanted to be a big part of the commercial launch industry and saw the opportunity through the U.S. fumbles. And you did it!

But seriously, how badly do you want space sovereignty?

Like almost all things in life, things are more complicated than they appear. If you’re interested in the complexities and want a consultation, please contact me through LinkedIn.

If you liked this analysis (or any others from Ill-Defined Space), please share it. I also appreciate any donations (I like taking my family out every now and then). For the subscribers who have donated—THANK YOU from me and my family!!

Comments ()